The traditional financial roadmap usually follows a linear path: work, save, invest, and eventually sell those investments to fund your lifestyle or new ventures. However, for high-net-worth individuals, entrepreneurs, and sophisticated investors, selling is often the least efficient way to access liquidity.

Every time you “exit” a position to fund a new opportunity, you face two significant headwinds: immediate capital gains taxes and the permanent loss of future compounding. This creates a “liquidity trap” where wealth is locked in assets that you are afraid to touch.

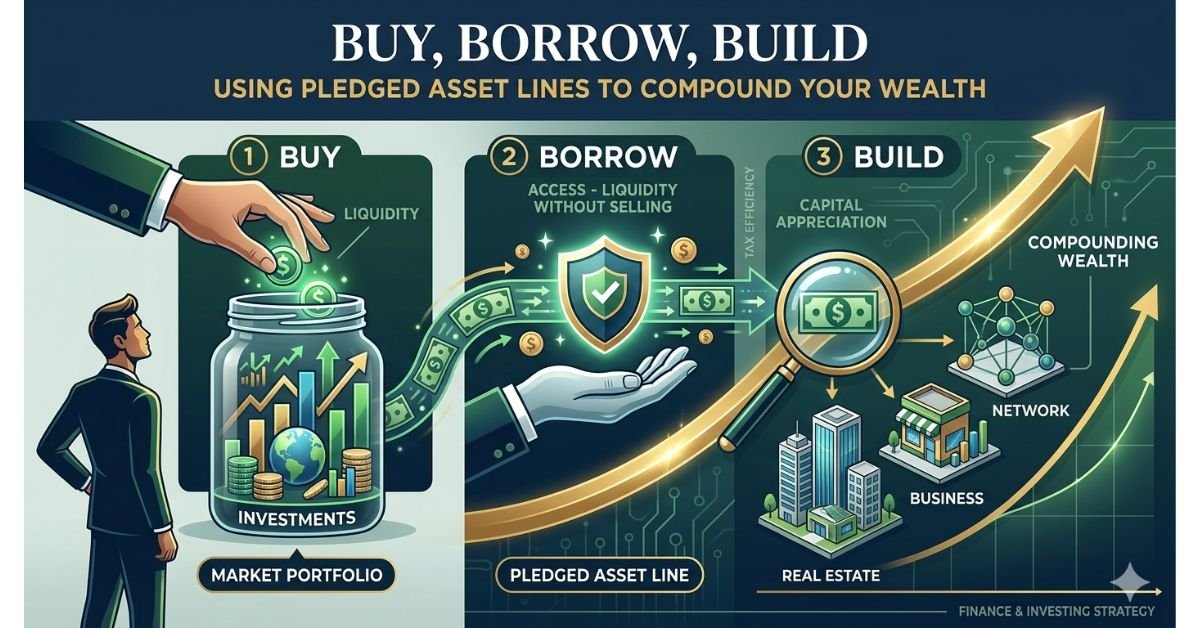

The “Buy, Borrow, Build” strategy, a favorite of the ultra-wealthy, solves this by utilizing a powerful but often overlooked tool: the Pledged Asset Line (PAL).

To understand the value of a PAL, one must first understand the true cost of selling. When you sell $500,000 of appreciated stock to fund a real estate deal, you aren’t just spending $500,000.

- The Tax Friction: Depending on your jurisdiction and holding period, you could lose 15% to 30% of that value to capital gains tax instantly.

- The Compounding Gap: If that $500,000 was growing at 8% annually, over 10 years, that capital would have been worth over $1 million. By selling, you forfeit that entire growth curve.

By borrowing against the asset instead of selling it, your original $500,000 remains in the market, continuing to compound, while you use the bank’s money to build your next venture.

A Pledged Asset Line is a non-purpose line of credit secured by the securities in a brokerage account. Unlike a standard “margin loan”, which is typically restricted to purchasing more securities, a PAL is designed to provide “out-of-plan” liquidity.

When you open a PAL, you pledge a portion of your portfolio (stocks, bonds, ETFs, or mutual funds) as collateral. The lender determines a “Loan-to-Value” (LTV) ratio based on the volatility and liquidity of those assets. For example:

- Equities: Typically have an LTV of 50% to 70%.

- Investment Grade Bonds: Can have an LTV as high as 80% to 90%.

Once established, the PAL acts like a revolving door of credit. You only pay interest on what you use, and the rates are usually pegged to a benchmark like SOFR (Secured Overnight Financing Rate) plus a small spread.

The “Build” phase is where this strategy separates itself from simple consumer debt. You aren’t borrowing for depreciating assets; you are borrowing to accelerate wealth.

In competitive real estate markets, cash is king. An investor can use a PAL to make a cash offer, closing the deal in days. Once the property is secured, they can put a traditional mortgage on the property to pay back the PAL. This “bridge financing” allows for speed without needing a literal pile of cash sitting in a checking account.

For business owners, a PAL can provide working capital or funds for an acquisition without the need for high-interest business loans or giving up equity to VCs. Because the loan is secured by your liquid portfolio, the bank’s underwriting process is significantly faster than a traditional commercial loan.

If you face a large, unexpected tax bill, selling stock during a market dip to pay it is a double loss. Using a PAL allows you to pay the IRS immediately while keeping your positions intact for the eventual market recovery. You can read more about the technical nuances of managing these credit lines inthis guide on pledged asset lines.

Not all debt is created equal. Here is how the PAL stacks up against other popular liquidity tools:

| Feature | Pledged Asset Line (PAL) | Home Equity Line (HELOC) | Margin Loan |

| Collateral | Marketable Securities | Real Estate Equity | Securities |

| Speed to Fund | 3–7 Days | 30–45 Days | Instant |

| Usage | Anything but buying stock | Anything | Usually buying more stock |

| Tax Deductibility | Often limited | Limited to home info | Often deductible vs gains |

| Closing Costs | Usually $0 | Appraisals & Title fees | $0 |

The PAL wins on speed and flexibility, making it the superior choice for time-sensitive investment opportunities.

No strategy is without risk. The primary danger of a PAL is the market’s inherent volatility. If the value of your pledged securities drops below a certain threshold, the lender will issue a maintenance call (commonly known as a margin call).

If this happens, you must:

- Deposit more cash.

- Pledge more securities.

- Sell assets to pay down the line.

To avoid this, sophisticated investors never “max out” their PAL. A common rule of thumb is to never borrow more than 25% to 30% of the portfolio’s value. Even in a significant market correction (a 30–40% drop), a portfolio leveraged at only 30% is unlikely to face a forced liquidation.

The “Buy, Borrow, Build” framework isn’t just about spending money; it’s about capital efficiency. It allows you to be in two places at once: your money stays in the market to capture long-term growth, while your credit works in the real world to capture new opportunities.

By shifting your mindset from “selling to spend” to “borrowing to build,” you turn your brokerage account from a static retirement fund into a dynamic engine for wealth creation.