Pakistan’s beauty and personal care market tells a story that investors and retailers are beginning to pay serious attention to. With a population exceeding 240 million, a median age below 23, and an urban middle class expanding at a pace that outstrips most comparable emerging markets, the structural conditions for consumer growth are firmly in place. The question is no longer whether this market will grow—it is which categories will capture the most value. Korean skincare is emerging as a compelling answer.

Pakistan’s broader beauty and personal care sector has been expanding at rates that consistently outpace GDP growth, driven by urbanisation, rising female workforce participation, and the rapid adoption of digital commerce. Within this market, premium skincare—a segment that barely existed five years ago at meaningful scale—is growing at double-digit rates annually, fuelled by a generation of consumers willing to spend more per product in exchange for proven efficacy.

The K-Beauty segment sits at the intersection of two powerful trends: the premiumisation of skincare consumption and the shift toward e-commerce as the dominant retail channel for beauty products. This intersection creates a favourable unit economics profile for retailers who get the sourcing, curation, and distribution model right.

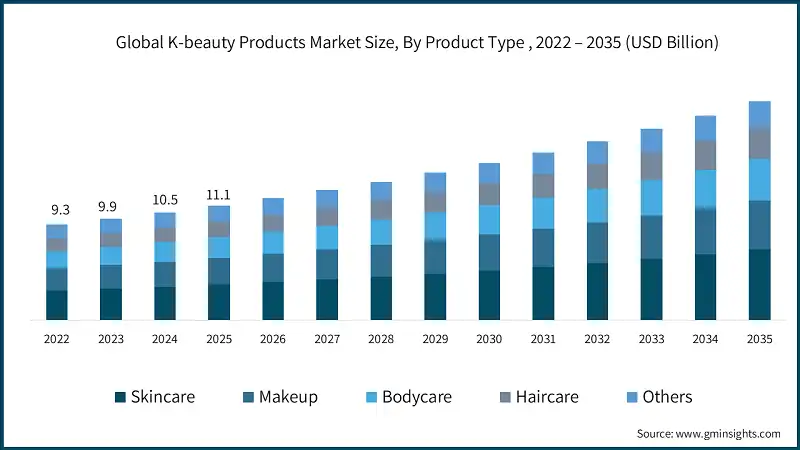

Globally, the K-Beauty market has surpassed $15 billion and is projected to exceed $20 billion by decade’s end. The fastest growth is no longer in the mature markets of North America or Europe but in emerging economies across South and Southeast Asia, where young, digitally connected consumers are adopting Korean skincare routines at accelerating rates.

Historical spending data in Pakistan’s beauty market reveals a clear generational divide. Older consumer cohorts allocate beauty budgets primarily toward colour cosmetics and basic personal care. Millennials and Gen Z, by contrast, are shifting spending toward skincare—and specifically toward products with identifiable active ingredients and transparent formulation claims.

This spending shift maps directly onto K-Beauty’s product proposition. Korean skincare brands have built their market position globally on ingredient specificity and step-based routines that encourage multi-product purchases. The average K-Beauty consumer buys more products per routine than a consumer using traditional Western skincare, creating a higher lifetime value per customer for retailers who capture this segment early.

The willingness to spend extends beyond products themselves. Pakistani consumers in this segment also invest time in education—researching ingredients, following skincare creators, and participating in online communities. This engaged behaviour translates into lower marketing costs for retailers, as organic word-of-mouth and community-driven advocacy replace expensive traditional advertising. For brands and retailers operating in this space, the customer acquisition economics are meaningfully better than in categories where brand awareness must be purchased through paid media alone.

Pakistan’s e-commerce infrastructure has matured significantly. Digital payment adoption has accelerated, last-mile logistics networks now reach second and third-tier cities, and consumer trust in online purchasing has increased steadily since the pandemic period. E-commerce penetration in Pakistan, while still below regional leaders, is growing at compound annual rates that rank among the highest in Asia.

For K-Beauty specifically, e-commerce solves a distribution problem that traditional retail could not. Korean skincare products require curated merchandising—ingredient education, routine guidance, skin-type matching—that physical retail environments in Pakistan rarely provide. Digital platforms can deliver this educational layer at scale. Established Pakistani e-commerce platforms expanding into K-Beauty have invested in category-specific content strategies that bridge the knowledge gap between curious first-time buyers and confident repeat customers, driving conversion rates that outperform general beauty categories.

The K-Beauty segment in Pakistan is still in an early growth phase, which creates genuine first-mover advantages for retailers who establish supply chain relationships, build consumer trust through product authentication, and develop the curatorial expertise to select products suited for the South Asian consumer.

The competitive moat in this category is not built through aggressive pricing or marketing spend. It is built through authenticity verification, product curation, and consumer education—capabilities that take time to develop and are difficult for latecomers to replicate quickly.

Retailers and investors evaluating this segment should focus less on current revenue and more on the structural indicators: category growth rates, repeat purchase behaviour, customer acquisition costs through organic content, and the competitive density of the market. By all of these measures, K-Beauty in Pakistan represents an early-stage opportunity with meaningful upside and defensible positioning for those who move decisively.

The parallel with K-Beauty’s trajectory in Southeast Asian markets is worth noting. In Indonesia and the Philippines, Korean skincare moved from a niche import category to a mainstream retail segment within approximately four years of adequate e-commerce infrastructure being established. Pakistan’s e-commerce maturation timeline suggests it is entering a comparable acceleration phase now. Retailers who build category expertise and supply chain capabilities during this window will be positioned to capture disproportionate value as the market scales—a classic early-mover dynamic in emerging consumer categories.