An accounting malpractice claim can severely harm a business and its reputation. It can go overlooked due to its complexity and its difference from errant mistakes. Complex dealings, unrecorded statements, and bookkeeping negligence are all ways it can be overlooked. To owners and stakeholders, accounting malpractice can lead to fraud and other legal complications; therefore, they must be able to spot potential cases to best avoid economic damages.

Financial statements are governed by principles that offer a business the ability to make decisions. These decisions range from determining the direction a business takes, therefore implementing alterations or additions to the business practices, and assuring compliance with implementing laws at the local and federal levels. When malpractice takes place, the information that is supposed to be in the hands of a stakeholder is modified or missing. This can lead a business to take inefficient and unjustifiable actions. Resources can be wasted. The stakes in this case are the legal actions a business can face. Managing a stakeholder’s confidence and a business’s financial stability is critical.

An accounting malpractice occurs when an accounting professional abdicates his or her duty to the profession by negligence or intentional misconduct. Examples of negligence can be recording transactions improperly, failing to reconcile accounts in a timely manner, and failing to report. Negligence, regardless of whether it is intentional or not, has serious consequences when mistakes are not corrected.

Deliberate wrongdoing happens when someone does something bad intentionally, such as forgery, record tampering, jumping the gun on reporting profits, or hiding losses. Making false or misleading statements is illegal, and that person can be subject to civil or criminal penalties and/or imprisonment. This is unlawful, and if a business is facing a risk, both financially and legally, they should contact a person familiar with legal & accounting malpractice laws to protect themselves.

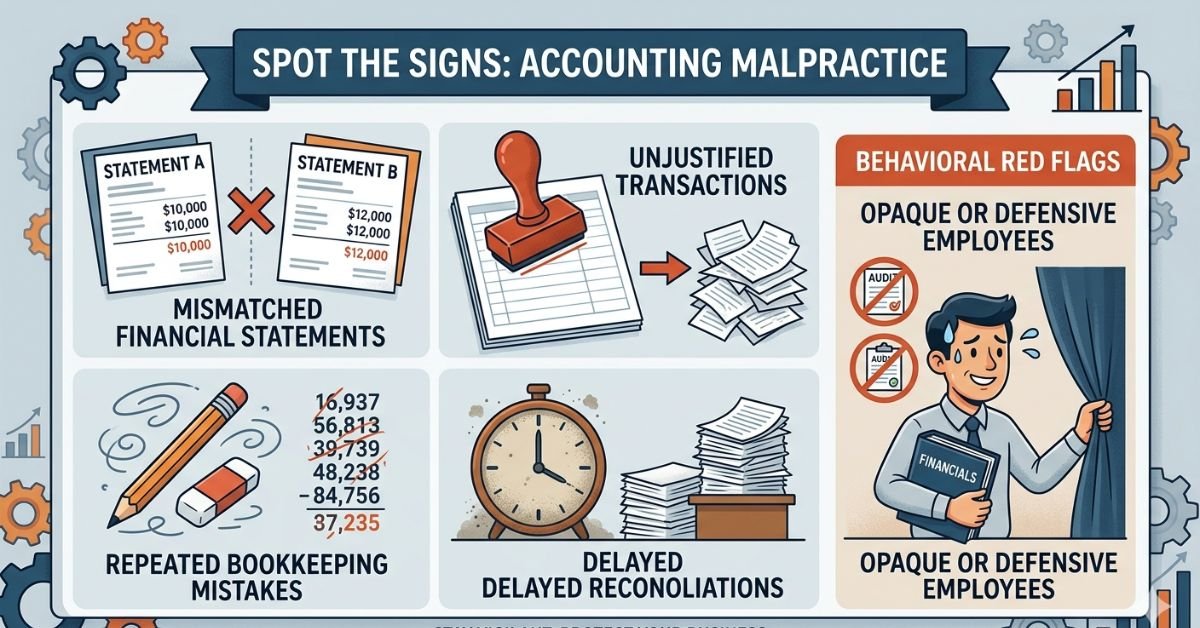

To detect malpractice, you need to be vigilant with both the numbers and the actions. The following are common signs:

- Financial statements don’t match: A number of reports have different numbers that are not normalized.

- Unjustified transactions: An entry that has no backing or penalties and/or justification.

- Mistakes in bookkeeping: Repeated mistakes usually lead to negligence or fraud.

- Reconciling delays: Accounts are not reconciled or reconciled infrequently.

- Opaqueness: Staff go to great lengths to avoid explaining anything.

Recognizing the warning signs allows a business to take preventative actions to solve serious issues.

Accounting negligence is a lot more than a simple mistake, and employee actions can be behaviorally proof of that. An employee that is non-compliant with behavioral audits, resists independent reviews, or gets defensive when questioned about the financial documentation or reports is likely to conceal something that is irregular or problematic. This is also true for the negligence or purposeful misconduct when an employee refuses to provide documentation that is supporting invoices, reconciliations, etc. The behavioral evidence, alongside financial evidence, is a good tool for a company to be more proactive in dealing with issues of malpractice.

Impact on Businesses Legal issues with businesses accounting cost legal issues such as civil court issues that can cost a ton of money. These issues can be a loss of a business’s reputation or loss of a cash flow business issue. There can also be loss of trust with clients or in whether the business will get investors again. There is a lot at stake with accounting malpractice, including trust issues and making sure there is no malpractice, which is important so money lost won’t be lost and to keep trust in the business.

There are some practical prevention measures that will aid businesses and can come in the form of:

- Internal controls: Clear process documentation with steps to avoid errors or limits on the process to avoid manipulation of the process.

- Regular auditing: To avoid or eliminate discrepancies, audits can be done before or after.

- Accounting staff—Hiring vested accountants and training them are requirements.

- Compliance programs—legal, accounting, ethical, guideline, or rule-based.

Anticipative strategies create greater confidence and malpractice prevention for all stakeholders. Businesses that manage and solve disputes safely within the boundaries of the law regarding accounting malpractice have an advantage.

Accounting malpractice is more than the math being done incorrectly; it is a betrayal of trust, certainty, and the progress of a business. Businesses can protect their position legally and financially by being proactive to fraudulent activities that are a byproduct of the existing holes in the system. A solid organizational system of audits, internal controls, and qualified personnel creates the atmosphere for a transparent culture. Professional consultation in accounting malpractice law enables a business to balance the complex needs of dispute management, resource protection, and trust of the stakeholders.